Education

Judicial vs Non-judicial foreclosure. 4 things investors must know

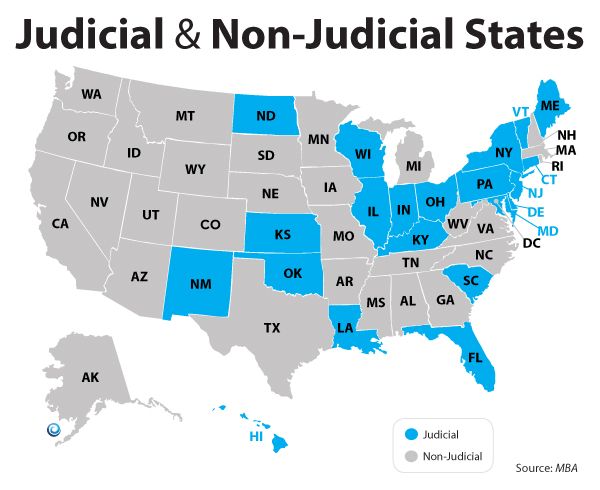

There are two types of foreclosure: judicial and non-judicial. One is much more expensive, time consuming. Investors beware states that force...

In the United States, there are two main types of foreclosure: judicial foreclosure and non-judicial foreclosure. Both types involve the lender repossessing a borrower's property in order to recover the amount owed on a mortgage loan. However, the process for each type of foreclosure is slightly different.

- What is Judicial Foreclosure?

Judicial foreclosure is the process that takes place in states where the lender must go through the court system to foreclose on a property. This type of foreclosure is typically slower and more costly than non-judicial foreclosure, as it involves the lender filing a lawsuit and obtaining a court order.

The process of judicial foreclosure typically begins when the borrower defaults on their mortgage loan. This can happen when the borrower fails to make the required payments, violates the terms of the mortgage agreement, or otherwise breaches the contract.

Once the borrower has defaulted, the lender will send a notice of default or "NOD" to the borrower, informing them that they have a certain period of time to cure the default. If the borrower is unable to cure the default within the specified time period, the lender may file a lawsuit to begin the foreclosure process.

Once the lawsuit has been filed, the court will set a hearing date and notify the borrower. At the hearing, the borrower will have the opportunity to defend themselves and present any evidence or arguments as to why the foreclosure should not proceed.

If the court determines that the borrower is indeed in default and that the lender has the right to foreclose, it will issue a judgment of foreclosure. This allows the lender to take possession of the property and sell it at a sheriff's sale.

The sheriff's sale is a public auction where the property is sold to the highest bidder. The lender is typically the first bidder and can bid up to the amount owed on the mortgage loan. If the property does not sell for at least the amount owed, the lender can apply to the court for a deficiency judgment, which allows the lender to seek the remaining balance from the borrower. - How does non-judicial foreclosure work?

Non-judicial foreclosure, also known as a "trustee's sale," is the process that takes place in states where the lender does not need to go through the court system to foreclose on a property. This type of foreclosure is typically faster and less costly than judicial foreclosure, as it does not involve a lawsuit.

The process of non-judicial foreclosure typically begins when the borrower defaults on their mortgage loan. As with judicial foreclosure, the lender will send a notice of default to the borrower, informing them that they have a certain period of time to cure the default. If the borrower is unable to cure the default within the specified time period, the lender may proceed with the foreclosure.

In a non-judicial foreclosure, the lender does not file a lawsuit. Instead, the lender appoints a trustee, who is typically a third party such as a lawyer or a title company, to handle the sale of the property.

The trustee will send a notice of sale to the borrower and publish the notice in a local newspaper. The notice of sale will contain information about the property, the amount owed on the mortgage, and the date and time of the sale.

The sale of the property takes place at a public auction, similar to a sheriff's sale in a judicial foreclosure. The lender is typically the first bidder and can bid up to the amount owed on the mortgage loan. If the property does not sell for at least the amount owed, the lender may not seek a deficiency judgment against the borrower. - What exactly is pre-foreclosure?

Keep in mind that the period from the filing of a NOD, sometimes referred to as a notice of intent to foreclose, kicks off what is commonly referred to as "pre-foreclosure". While pre-foreclosure is not an official legal status, this intermediate phase between NOD and judgement is what is being referenced. So, when you create a lead list on REISkip's list builder, and you use the pre-foreclosure filter, any property along that continuum is an eligible property for that list.

Since there are multiple steps along the path to a foreclosure, there are different schools of thought about when is the best time to contact a homeowner in distress.

As the name suggests, an NOD is simply a notice from the lender to the borrower, that they are in default on their mortgage and that the bank may execute its right to foreclose. Some investors believe that contacting the borrower at this early stage preserves the most options and minimizes the accumulation of arrearage in the event they are able to work out an arrangement with the homeowner. That said, an NOD is so early that it may not be a good indication of true distress.

As a result, some investors will only pursue distressed properties where the official legal process has begun. The first court filing is called a lis pendens. A lis pendens is a public notice that is filed with the court and recorded in the county land records, indicating that a lawsuit affecting the title to real property is pending. Once a lis pendens has been filed, the foreclosure process begins in earnest. It is at this point that many homeowners will begin to seriously evaluate their options. - What is the impact on investors in judicial foreclosure states?

The impact on investors can vary depending on what strategy you are pursuing. If you are a wholesaler, the timing considerations are the most relevant, as you will need to gauge how close the delinquent homeowner is to an actual consummated foreclosure.

If you are a note investor or you are structuring wrap mortgages or other creative structures where you could need to foreclose, you are essentially the bank. You will have the same considerations other lenders do as you evaluate the time and risk associated with foreclosing on non-performing loans. Those strategies, when executed in judicial foreclosure states, will likely face longer wait times. You must account for this and include the additional cost in your contingency budget from the outset. Be sure budget for the additional time as well, as there will like be an extended period of non-payment as the process meanders through your state's court system.

It is difficult to estimate the average cost of a foreclosure action in a judicial foreclosure state, as it can vary significantly depending on a number of factors, including the location of the property, the complexity of the case, and the fees charged by the court and any attorneys involved.

Obviously, attorneys fees can vary wildly, but a good starting point is Fannie Mae's published guidelines for servicing foreclosure action on properties with Fannie mortgages. This is a state by state schedule of maximum allowable attorneys fees. Keep in mind that this has no bearing on what can be charged to foreclose non-Fannie properties.

Also, keep in mind that this is just one of the out of pocket expenses that lenders incur in servicing foreclosure actions. There are several others, as well as the cost of lost time and other intangibles.

Click the button below to use the REISkip list builder and create your first foreclosure or pre-foreclosure lead list. We have millions of records, compiled from data in both judicial and non-judicial states.

States that are Non-Judicial:

The following states are non-judicial states, meaning that lenders in these states may use the non-judicial foreclosure process: Alaska, Arizona, California, Idaho, Minnesota, Montana, Nebraska, Nevada, North Dakota, Oregon, South Dakota, Utah, and Washington

Start Skip Tracing

Ready to get actionable data to help you close your next deal?

Sign up for your free account today!

Learn

Helpful Resources

REISkip is more than just a product. We partner with the best data scientists, technologists and real estate leaders to bring you the latest in trends and industry knowledge to supercharge your business.